Which city leads our prime price forecast?

Plus, Golden Visas are alive and well

4 minutes to read

Forecast

This week we launched our prime global city forecast. A lot has changed since we last took the pulse of prime markets in December 2022.

New Zealand has seen four additional rate rises taking its tally to 12 hikes, Canada has introduced a ban on foreign buyers, Los Angeles’s Mansion Tax is up and running, and Singapore has ramped up stamp duty for non-residents from 30% to 60%.

It seemed an opportune time therefore to ask our global research teams to dust off their crystal balls and provide us with their take on the risks and opportunities facing their luxury housing markets and crucially, where they think prime prices are headed.

Of the 26 cities tracked, in 2023 six cities are expected to perform more strongly than predicted six months ago, the forecast for nine markets remains unchanged, while the remaining eleven will see weaker price growth than previously envisaged. View the full city rankings here.

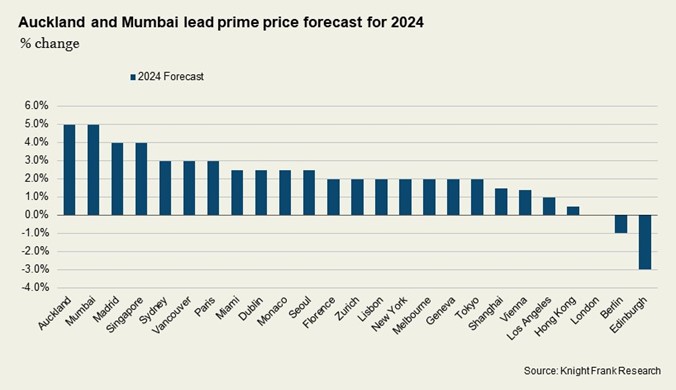

For 2024, Auckland and Mumbai lead the forecast, both tipped to see 5% growth over the 12-month period. Auckland is moving into recovery mode having seen prime prices dip 17% since its peak in Q3 2021.

In Europe, Madrid (4%), Paris (3%) and Dublin (2.5%) are expected to be the top performers, a lack of luxury stock and relative economic resilience explain the positive outlook in these cities. For more on Madrid’s economic and eco-credentials read our deeper dive here.

Golden Visas

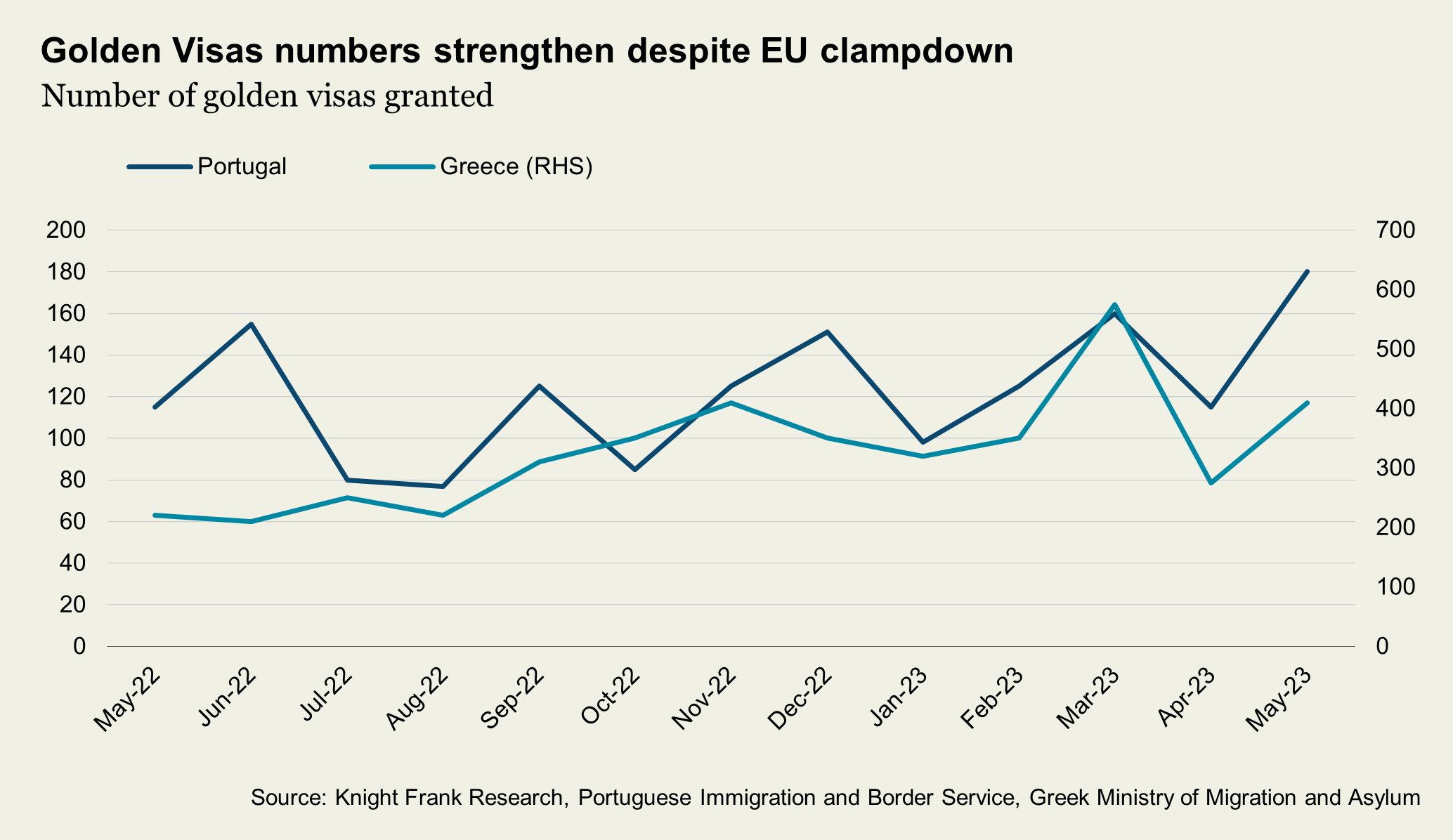

New data suggests that contrary to the EU’s efforts the golden visa landscape is booming.

In Greece and Portugal, the number of visas granted in recent months has been on the up, and demand in Italy and Spain has hit record levels according to research by Bloomberg.

The EU has urged members to shut down such initiatives for fear they facilitate money laundering. The UK and Ireland have acted already closing their schemes, Portugal has switched its focus from real estate to capital investment and Greece has upped its property purchase threshold from €250,000 to €500,000, but the programmes continue to attract strong demand. Our Algarve Insight Report analyses the Portuguese Golden Visa further, amongst a wider market overview.

The data suggests whilst policymakers talk of tighter restrictions, the legislation isn’t mirroring their tough talk.

The 180 golden visas granted in Portugal in May represents a several year high according to Bloomberg, whilst Greece’s figure of 412 is a 87% increase from the previous year.

But as we discuss in our latest A Home Abroad webinar the recent flurry of new digital nomad visa announcements now offer the untethered freelancer a means to stress test their chosen location before taking the leap of applying for residency and the outlay that comes with it, whether a property purchase, business set up or lump sum investment.

US

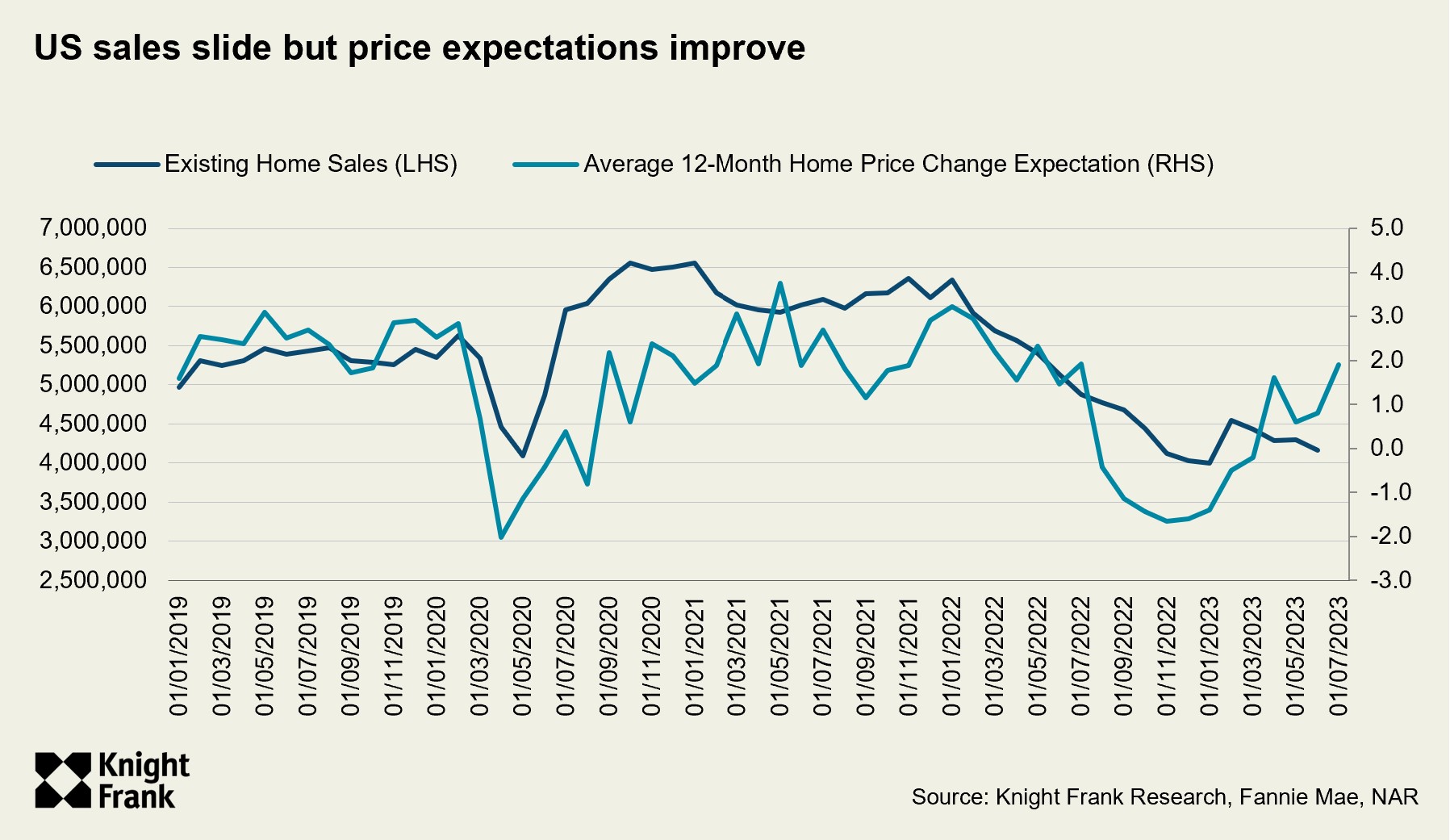

Last month we talked about how the US looked to be achieving its goal of a soft landing, data released in the last few weeks further supports this view. Inflation has receded to 3.3% and at the same time jobs and wage growth are strengthening at a modest pace. But housing is a pinch point.

Dig into the inflation numbers and they reveal that “shelter inflation” or in other words, rents, hotels and lodgings were responsible for 90% of the US Consumer Price Index’s monthly gain last month.

New York luxury rents are still rising at an annual rate of 10.3% according to Knight Frank’s Prime Global Rental Index and prime prices across the major three US cities we track, New York, Miami and Los Angeles, are down only 0.4% on average from their pandemic peak, despite the US 30-year fixed rate mortgage nudging 7.2%.

This price resilience is attributable to a lack of inventory driven by US homeowners opting to stay put rather than incur a hefty mortgage hike.

The result is sales and prices are diverging.

Existing home sales fell 19% year-on-year in June to 4.16 million and the number of purchases by foreign buyers also declined. International buyers bought around 85,000 US homes between April 2022 and March this year, the fewest since this data was first tracked in 2009.

In contrast, Fannie Mae’s Home Purchase Sentiment Index confirms the net share of those who say home prices will go up in the next 12 months increased 6 percentage points month-on-month in July.

Europe

The challenge for EU policymakers is switching from containing inflation to maintaining economic growth.

The IMF expects the EU to narrowly avoid a recession, forecasting 0.9% growth in 2023, this will inevitably influence wealth creation.

Interest rates across the Eurozone are forecast to top out at 4.0% according to Capital Economics, that means one more hike is likely between now and year-end, most likely in September.

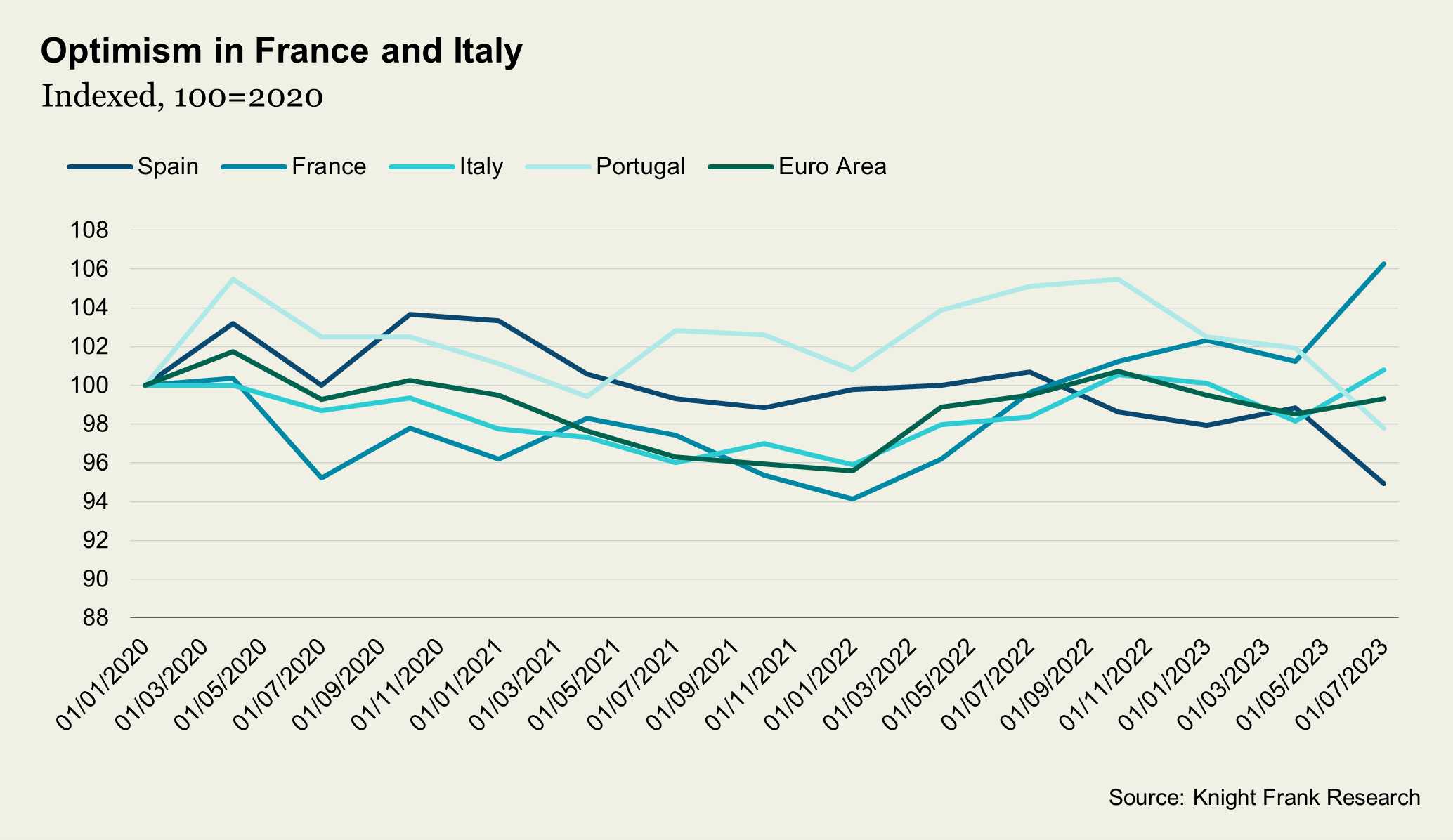

The narrative that the bloc is ‘nearing the peak’ looks to be filtering through to consumer sentiment with households in France and Italy amongst the most confident about buying or building a new home in the next 12 months.

Knight Frank’s latest Prime France series of reports reflect this positivity, with Paris in particular primed for heightened activity with large-scale infrastructure improvements and its hosting of the 2024 Olympics. Read more here.

In other news

US mortgage rate climbs to 7.16%, matching highest since 2001 (Bloomberg), China home prices drop at faster pace as downturn worsens (Bloomberg) and the draw of alternative international schools (Financial Times)